Correcting a Decade of Over-Taxing New Housing

How governments are starting to reverse the policies that priced out middle-class homeownership

Highlights

After years of policy inertia, the federal government and the province of Ontario are finally moving in the right direction, albeit with temporary measures: an HST rebate on new homes and reductions in development charges could cut new-home prices in Ontario by 10–20%, aligning with long-standing MMI recommendations.

These moves address the current climate, where resale prices have fallen while construction costs haven’t, leaving us in a perverse equilibrium where homes are still too expensive to buy but not profitable enough to build.

In a real-world example, these reforms could lower the minimum viable price of an entry-level Oshawa townhome from about $730,000 to roughly $615,000, a meaningful 16% drop that could bring stalled projects back to life.

This is a good first step, but not a solution. Even at $615,000, many middle-class families are still priced out, and without deeper structural reform to taxes like development charges, governments will continue to treat new homebuyers as a revenue source rather than a policy priority.

And let’s be clear: this isn’t a “subsidy.” Even after these changes, buyers are still paying tens of thousands in taxes. The real issue is that housing taxes, particularly development charges and HST on new homes, have grown far beyond any reasonable connection to actual costs, and are now a primary driver of unaffordability.

If housing is a human right, or at least a necessity, we need to ask ourselves why a young family buying an entry-level home is assessed HST, while caviar and foie gras are considered a “basic necessity” under tax law and are exempt from HST. If a simple home to raise a family isn’t a basic necessity, what is?

Finally, some housing relief… though some details TBD

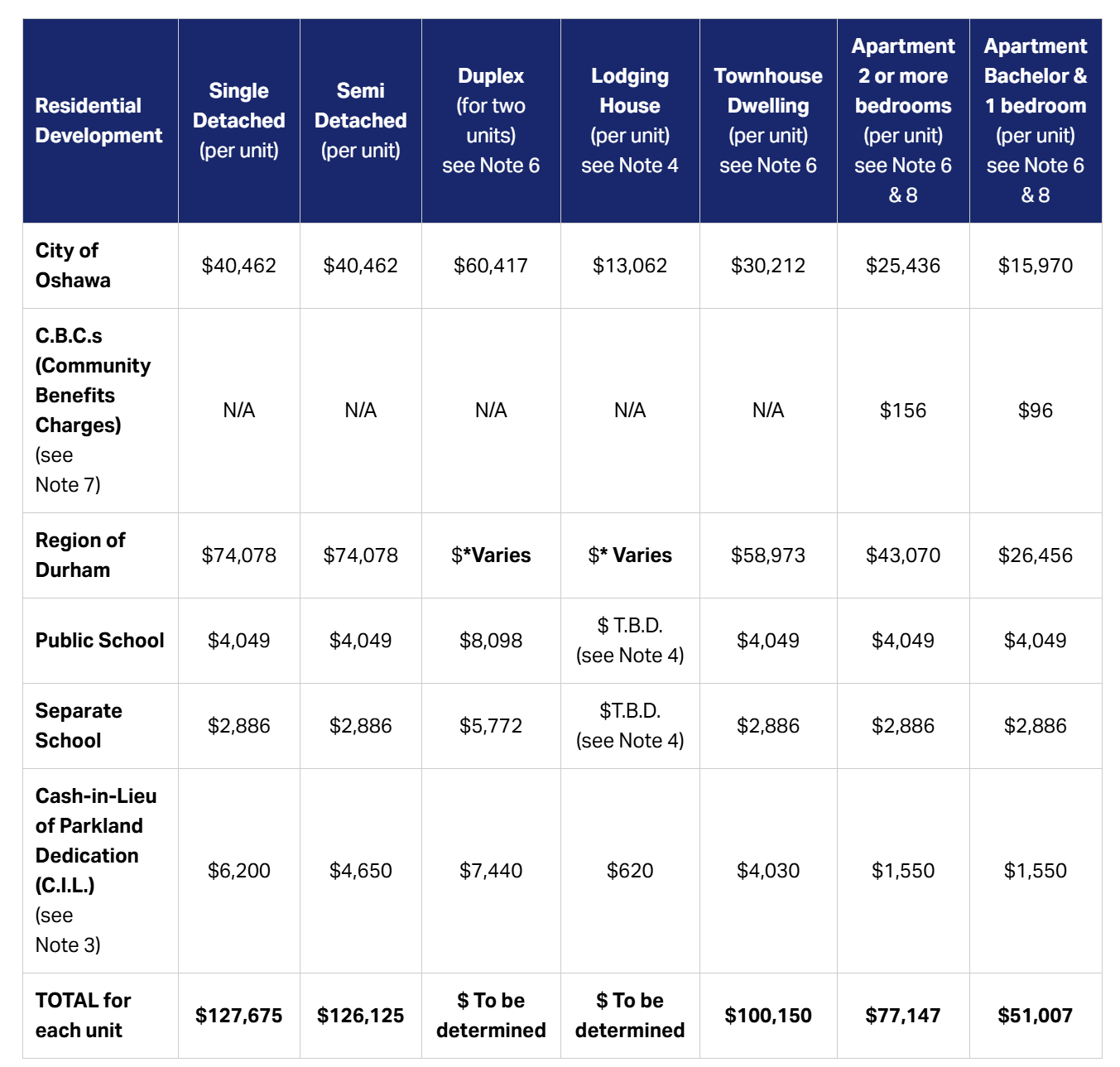

In the past two weeks, the federal government and the province of Ontario have reached two agreements, both of which align with recommendations in several MMI reports, which combined will lower the price of a new home by as much as 20%. The first announcement is a one-year enhancement of the HST New Housing Rebate and New Residential Rental Property Rebate that will rebate all HST on homes priced under $1 million, with a partial rebate for homes priced under $1.5 million, which can remove more than $100,000 in HST from the cost of a new home. The second announcement is a three-year reduction in development charges of up to 50% for some homes in some Ontario municipalities. Details on this plan are still relatively sparse, including timing and size of the reduction for any particular home, but the federal government and the province have each allocated $4.4 billion to the fund.

Ontario finds itself in a strange equilibrium, where the price of resale homes has substantially fallen, creating affordability, while the costs of building new homes have not. Benjamin Tal of CIBC summarized it best when he said, “Home prices are still too high to buy and not high enough to build.” Lowering development charges and rebating HST, which applies only to new homes, will lower the cost of homebuilding, leading to both lower prices and increased construction activity.

While these moves will not end the housing crisis and are both temporary, they will help move the needle and make housing more attainable to young, middle-class families. While all the details have not been released, here is what an HST rebate and a 50% reduction in development charges would mean for the construction of an entry-level family-sized townhome in the City of Oshawa.

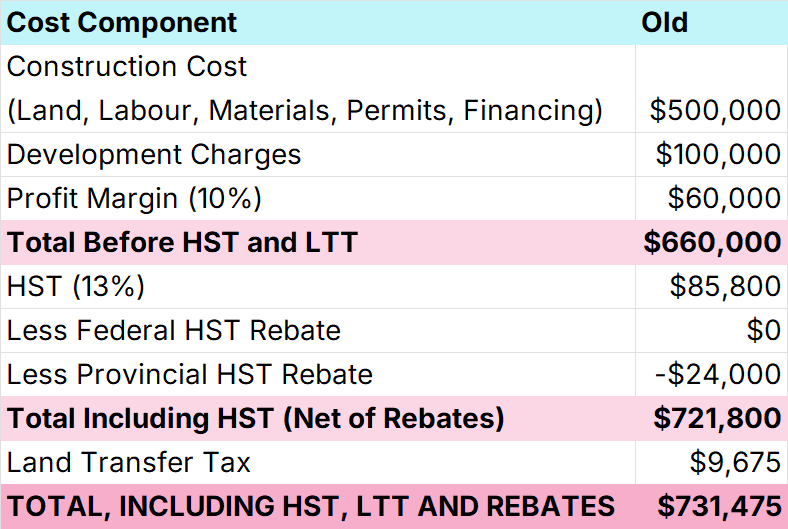

Before the reforms: A $730,000 townhome price floor

Let’s take a highly simplified example of a developer who wishes to build an entry-level townhome in Oshawa, and the potential purchaser is not a first-time homebuyer. The developer’s cost to build, including land, materials, labour, financing, permits, but excluding development charges, is $500,000 a unit. Currently, development charges for this type of unit, are just over $100,000, as shown in Figure 1, which increases the costs to $600,000.

Figure 1: Development charge schedule for Oshawa, ON, as of April 2, 2026

Chart Source: City of Oshawa.

The developer will need to obtain construction financing for the project, and no lender will finance it if it has an insufficient profit margin, given the risk of non-payment. We will assume for this developer that they need to show a minimum 10% profit margin. This bumps the price up to $660,000.

A 13% HST is applied to the $660,000 price, adding an additional $85,800 in taxes to the project. While (under the old system), this project would not qualify for a federal HST rebate as the home price is too high, it would qualify for a $24,000 provincial rebate. After rebates, our HST-inclusive price is $721,800.

Finally, the buyer would have to pay an additional $9,675 in land transfer taxes on the project, which brings the cost to just over $730,000, as shown in Figure 2.

Figure 2: Cost breakdown of a hypothetical Oshawa condo project

Chart Source: MMI.

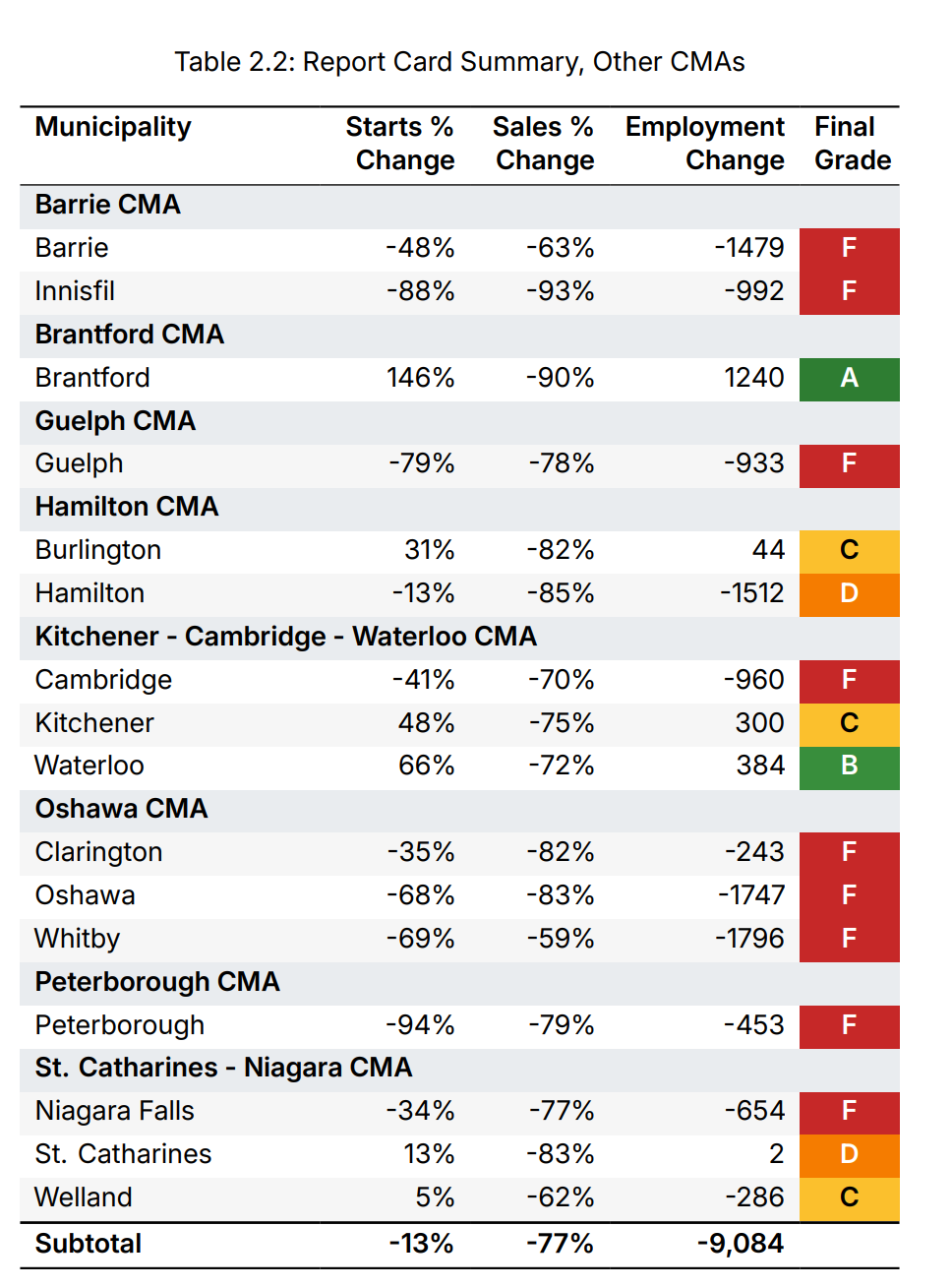

This is a highly simplified example and excludes several closing costs, but it is a useful estimate. The $731,475 figure represents the lowest possible price the developer could sell the unit for. If there is no market for townhomes at this price because resale prices for equivalent units are lower, then this home simply will not be built. This helps explain why pre-construction home sales in Oshawa are down by more than 80%, as shown in Figure 3.

Figure 3: Pre-construction sales changes by municipality, Q3 2025

Chart Source: The Big Collapse: New Condo Sales Down 89%, Ground-Oriented Down 65%.

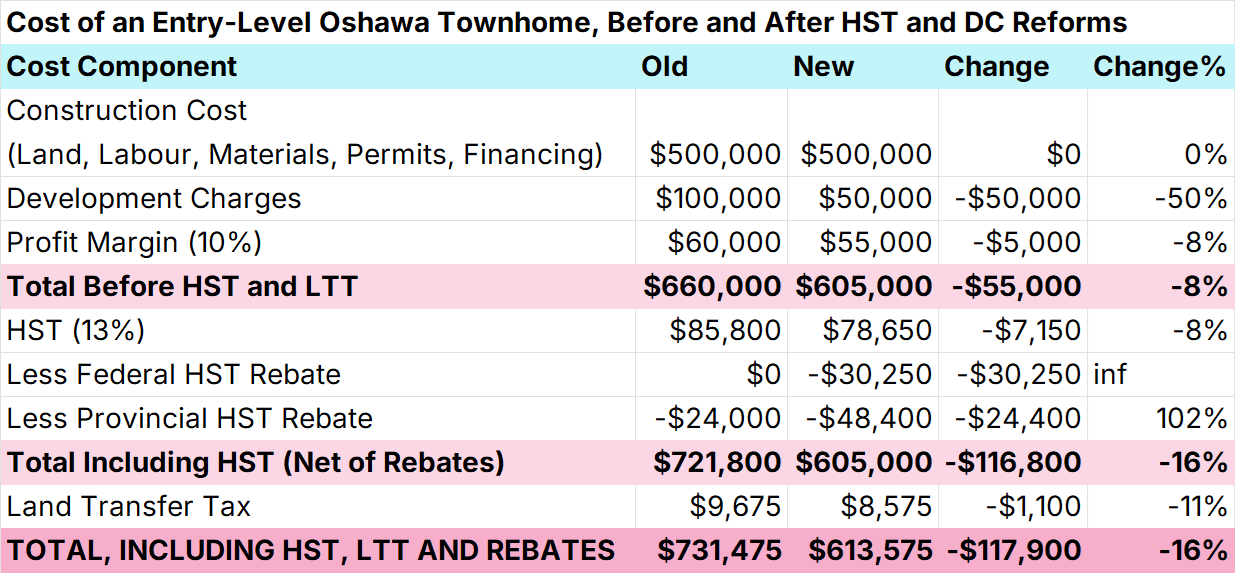

After the reforms: A $615,000 townhome is possible

But now let’s apply both a 50% reduction in development charges and a full 100% HST rebate to this project. This not only reduces DCs by $50,000 and eliminates HST payable, but it also reduces the amount of land-transfer tax payable and allows the developer to get construction financing at a lower profit margin (in dollar terms). It lowers the project’s minimum viable price to $613,575, a 16% reduction, as shown in Figure 4.

Figure 4: Cost breakdown of a hypothetical Oshawa condo project after a 50% DC reduction and full HST rebate

Chart Source: MMI.

This is a substantial reduction, and should allow more homes to be built, and sold to consumers at lower prices, as the market for new $614,000 townhomes is substantially higher than the market for $732,000 ones.

This is a fantastic joint initiative from the federal government and the province of Ontario, and I hope that it is replicated in other provinces with high development charges (looking in your direction, British Columbia). It is a sign that our governments are starting to take the home ownership crisis seriously.

This is the beginning of a process, not the end

There are, however, a number of factors and caveats we should keep in mind here:

We do not know for sure that the development charge reduction for this type of home will be 50%, we do not know when the reduction will take place, and we do not know if municipal governments will increase other fees by an offsetting amount, as has happened in the past (looking in your direction, Metro Vancouver). It is vital that governments move forward with implementation; we’ll be watching closely at MMI.

A price point of $613,500 remains out of reach for far too many middle-class families, so other reforms are needed to bring new home prices down to a level that young, middle-class families can afford. But we should not overlook the value of a 16% price reduction, which saves families $117,900.

It may be the case that this still isn’t a large enough reduction to get homes built, given current market conditions.

Alternatively, it is also possible (though given current market conditions we suspect unlikely) that this is a larger-than-needed reduction in costs, and some of these tax savings will not be passed along to consumers, but rather captured by some combination of developers through higher prices, landowners through higher land prices, labour through higher wages for the trades, sellers of construction materials through higher prices for drywall and toilets, and by lenders through higher construction loan interest rates. This is also something worth monitoring closely.

It is exceptionally difficult to estimate how many additional homes will be built due to these changes, as we discussed on last Friday’s episode. The most straightforward way to derive such an estimate (and to derive estimates for the previous point) is to apply elasticity parameters, which examine how quantity supplied and demanded change in response to a price change. However, those parameters would be generated from past market conditions, and our current market is unlike anything we have seen in decades. Elasticities are not constant and are certainly different today than they were 10 years ago.

While incredibly valuable, these are all temporary measures, and are not the kind of deep structural reforms Ontario needs to the development charge system, the kind we discuss in the report we co-authored with OREA, A Pathway to Development Charge Reform.

These deals only cover Ontario; other provinces with sky-high development cost charges and other taxes on housing construction still need to come to an agreement with the federal government (looking in your direction, British Columbia).

And there is one final elephant in the room that is worth mentioning.

These new rebates are not a subsidy; there are still nearly $60,000 in construction taxes on this home

There is a fair bit of chatter on social media, from Bluesky to Reddit, that these programs are a “subsidy” to homebuyers and developers. This is an understandable viewpoint, but it simply does not hold up to scrutiny. The homebuyer is still on the hook for nearly $60,000 in taxes ($50,000 in development charges and $8,575 in land transfer taxes). In contrast, the new home I bought in 2004 had only $17,000 in taxes (less than $5,000 in development charges, $7,500 in GST, $3,500 in PST, and $1,400 in land transfer taxes, which in my case were waived entirely because I was a first-time buyer). That is over a 250% increase in taxes in just over 20 years, and that’s after these so-called subsidies.

There is an assumption in this “subsidy” argument that the taxation levels on housing are just, normal, and necessary. But let’s first consider the HST. In Canada, basic necessities like basic groceries, prescription drugs, and medical devices are all exempt from the HST (or, more accurately, they are “zero-rated”). Which means when a 0.1% goes to buy caviar and foie gras, they are not charged HST on those purchases.

However, housing, which both international and national law consider a human right, is assessed for HST when an owner-occupant purchases a new home. So when our 0.1% buys caviar and foie gras, they’re fulfilling a basic necessity, but when a young couple buys a modest townhome to raise a couple of kids, that’s a luxury purchase and taxed as such?

Now you could respond with, “while housing is a human right, owning one isn’t… it’s a luxury when a family could always rent”. In that case, if ownership housing is a luxury, reserved only for the rich, we ought to ask why so many existing homeowners qualify for financial supports, such as Old Age Security, which is set to exceed $100 billion in annual expenditures by 2035.

We can certainly understand placing HST on “luxury homes”, but forcing a young couple buying a modest home to raise a couple of kids to pay HST on that purchase, while keeping caviar and foie gras tax exempt, is a choice.

Next, consider development charges. If development charges were simply defraying the direct cost of building a new home, they would not have risen by over 5000% in the City of Toronto over the past 25 years, as the cost of building infrastructure has not risen by that much.

The whole argument that development charges need to be this high because “growth should pay for growth” is based on a policy sleight-of-hand that confuses population growth with the growth of the housing stock. As I pointed out in a previous article, the building of the home I moved into in 2004, and my being able to move out of my parents’ home, did not give rise to additional expenses:

Moving to this home did not increase my library usage.

Moving to this home did not increase my use of local parks and facilities.

Moving to this home did not increase my use of city roads. In fact, my driving was significantly reduced because I was able to purchase a home closer to where I worked. High road usage is typically a sign of a lack of development, forcing people into long commutes.

And the infrastructure associated with the house, such as subdivision roads, sidewalks, sewers, and lampposts, is not funded by development charges. The developer (not the city) pays for the construction of those outside of the development charge system, and passes those costs along (with a markup) to the homebuyer. Annual property tax payments pay for their upkeep.

In short, the fact that a new home was built did not entail a significant increase in infrastructure costs for the municipality. People use libraries and roads, not homes, and making young people live with their parents well into their 30s, or in overcrowded, overpriced housing, does not reduce infrastructure use. Population growth creates the need for infrastructure, not housing growth.

We need to see development charges for what they are: a tax on new homebuyers, which pushes up the price of existing homes, used to support the costs of population growth, replace aging infrastructure, and buy nice things that existing homeowners would not pay for if they had to foot the bill themselves. Lowering these taxes is not a subsidy, as their rates do not reflect the costs of new housing development.

I am not arguing about reducing taxes on new houses, but I do believe the point about infrastructure needs to be further clarified.

In Calgary, we just wrapped another long hearing into blanket rezoning. One thing that has been referenced by some councilors during the hearing is that some inner city neighborhoods now have lower population than 20 years ago. So there, our infrastructure might be oversized relative to the population.

Is that a case to say that an inner city development that increases density is a much cheaper option than sprawling development? Not only in the long term but also in the short term?