Boosting Demand for New Homes Is Supply-Side Policy

Policies that favour old homes over new ones are quietly strangling supply

Highlights

Boosting demand for new homes is essential to increasing housing supply, as without sufficient demand, new housing projects won’t get built. Supply-side policy must begin with demand-side activation targeted at new homes, not existing ones.

Canada’s tax and regulatory systems favour existing homes over new construction. New homes face significantly higher construction taxes than those built 20 years or more ago.

To meet our housing targets, we must rebalance the system toward new construction. Policy must intentionally tilt the scales in favour of tax and regulatory reforms to encourage building.

An increase in demand for existing homes causes home price inflation. The solution to that inflation is to increase the supply of new homes. Policies, like GST reform, that incentivize new construction, are the answer. In other words, more generous GST rebates are the cure to home-price inflation, not the cause.

There’s no new supply without demand for new supply

We have received a great deal of thoughtful feedback on our pieces examining the reform of GST rebates on housing, which aims to save new homebuyers over $100,000.

These pieces tend to generate thoughtful e-mails and responses, with the pushback that “cutting the GST will just boost demand, the opposite of what we want. It will simply cause inflation in the housing market. Instead, we need policies focused on supply, if we have any hope of hitting our federal and provincial housing targets”.

To which, we respond: “There is no increase in new housing supply without increasing the demand for new homes. Supply requires demand. Policies that increase supply are the cure to inflation, not the cause.”

The key term in this response is “new”. Housing is an unusual product, as sellers (or landlords) of new housing must compete with the sales and rentals of existing homes. As we demonstrated in "New Homes Are the Solution: Policy Must Treat Them Differently," there is a fundamental distinction between increasing demand for new homes and increasing demand for existing homes.

Figure 1: Market responses to housing policies

Source: New Homes Are the Solution: Policy Must Treat Them Differently

Currently, our tax and regulatory systems are biased towards buying existing homes, rather than building new ones, which simultaneously slows housing growth while boosting the price of existing homes. Or, to adopt the analogy Mike used on a recent Missing Middle episode, our policies disincentivize the creation of new baseball cards and stoke the demand for 1967 O-Pee-Chee Mickey Mantle cards, a product that can no longer be made.

An increase in demand for existing homes causes home price inflation. The solution to that inflation is to increase the supply of new homes. In other words, more generous GST rebates are the cure to home-price inflation, not the cause.

There is no pathway to doubling housing starts without a rebalance of the system, away from buying up existing homes and towards building new ones. We must increase the demand for new housing.

Here are four (of many) ways policymakers can rebalance the system to give new housing construction a fighting chance.

1. Reforming taxes on housing construction and new home sales

When you buy a new home in Ontario, the construction and sale of that home are subject to a multitude of taxes, some of which, including (but not limited to) development charges, GST, and PST, are not charged to existing homes. This creates a natural biasing of the tax system towards buying existing homes and against buying new homes.

There is a counterargument to this logic, which states that although someone buying an existing home does not pay DCs, GST, and PST, the original purchaser did, and the costs the original purchaser paid are “passed along” in future sales.

Fair enough. But even if we adopt this logic, the housing construction tax system is currently highly biased against new homes. Here’s how.

Take this London, ON home that MMI Founder Mike Moffatt and his partner bought brand new in 2004 for $168,000.

Figure 2: Mike’s house

Source: LSTAR

There were three taxes Mike paid that are relevant to this discussion:

When he bought the house, development charges were around $5,000 ($7,800 in 2025 dollars).

Mike paid a then 7% GST, but had 36% of that rebated back to him under the GST New Housing Rebate, for a total GST expense of $7,500 ($11,700 in 2025).

There was no PST on new housing in 2004 (Mike is old), but there was PST on some of the building materials used in the construction of the house, which the Ontario government estimated to be around 2% of the cost of a new build. That is roughly $3,500 ($5,500 in 2025).

Added together, Mike would have paid $16,000 in DCs, GST, and PST, equivalent to $25,000 in 2025. These are the costs that Mike “passed along” to the buyer, and will get passed along to future buyers.

Now, let’s consider the option of buying a newly constructed home of this size in London, Ontario, which would cost at least $600,000 today. We’ll call it $600,000, and apply our three taxes to it:

Development charges on a single-detached home are currently $48,526.

The federal portion of the GST is now only 5%. However, at $600,000, the home is ineligible for a GST rebate since its value exceeds $450,000; therefore, the GST expense is $40,000 (5% of $600,000).

There is an 8% PST on this home, but it is eligible for a $24,000 PST rebate. The total post-rebate PST expense is $24,000 (8% of $600,000 is $48,000, which is reduced to $24,000 after a $24,000 rebate).

That is over $100,000 in DC, GST, and PST paid by the buyer, over four times the (inflation-adjusted) taxes on the home built in 2004. This only covers a subset of taxes and fees, and does not include tax-on-taxes or interest charges related to these fees.

If we want to increase housing construction, we cannot be taxing new homes at four times the rate of buying a pre-existing home built in 2004. The evolution of construction taxes and home prices has biased the system toward buying existing homes rather than new ones, which has slowed housing construction.

There are solutions to this, including reducing development charges and updating GST rebates to reflect 35 years of inflation in home prices. British Columbia, wisely, exempts new homes (under a certain price point) from property transfer tax charges to help level the playing field. Ontario could do the same with land-transfer taxes.

2. Eliminating capital restrictions on new housing construction

Canada instituted a foreign-buyer ban as the country was concerned about persons living outside of the country “buying up” existing units, crowding out the families that need them. Unfortunately, because this ban applies across the board to both existing and new homes, it has eliminated a crucial source of the $2 trillion in capital needed to meet our housing supply target.

There is a simple solution to this problem: Follow the lead of Australia, and exempt new housing from foreign-buyer bans. This tilts the playing field in favour of building housing, rather than buying existing.

The federal government should immediately undertake a study to identify all the ways Canada blocks or disincentivizes capital investment in real estate construction, such as EIFEL rules, and create policy fixes.

3. Make it more profitable to build new rental housing than to buy up existing single-family homes

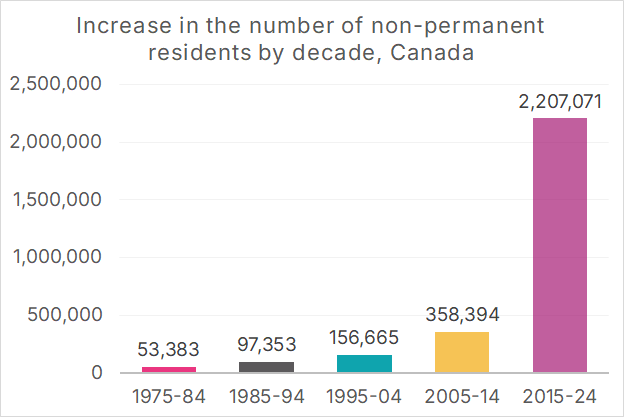

Our piece, “No 3-Bedroom Homes, No Kids, No Future: Why Families Are Leaving Cities,” painted a stark picture, showing how families with young children were priced out (or pushed out) of the GTA and Ottawa, as investors bought up single-family homes as a predictable response to government policies that brought hundreds-of-thousands of extra renters to the province.

Figure 3: Increase in the number of non-permanent residents by decade, Canada

Source: The Next Housing Minister Must Restore the Dream of Homeownership

While the province needs to increase the rental stock of all forms of housing as much as possible, this should primarily come from building new housing, rather than converting owner-occupied housing.

Changes in tax policies can help address this issue. The federal government fulfilling their campaign promise to reinstate the Multiple Unit Rental Building (MURB) cost allowance would help balance the tax system towards buy vs. build:

A MURB program allows individual investors in rental apartments constructed after a certain date to deduct expenses related to that building from their personal taxes. Most notably, it allows investors to flow-through depreciation onto their personal income taxes. This provision is particularly attractive in the current tax environment, as the Liberal government increased depreciation rates on rental apartments from 4% to 10% as part of Budget 2024. That move was designed to encourage investment in apartment construction and was a key recommendation of both the National Housing Accord and Blueprint for More and Better Housing. The synergistic effect of MURB, a 10% depreciation rate, and 2023’s elimination of GST/HST on purpose-built rental construction on creating a favourable tax environment for apartment construction cannot be overstated.

By creating tax benefits that can only be gained through building, rather than buying, we can accelerate housing construction. The federal government should study other policies that could have a similar effect, such as a version of the United States’ 1031 Exchange, but for the building of new rental housing.

4. Target incentives for homebuyers to purchase new, rather than existing homes

A wide range of programs, such as the Home Buyers' Plan, exist to help middle-class families achieve the dream of homeownership. While these programs can be useful, critics are not incorrect in noting that they increase the overall demand for housing, which in turn raises prices.

But what if we applied the logic of "New Homes Are the Solution: Policy Must Treat Them Differently" and created a suite of programs that only applied to the purchase of new homes as a way to stimulate housing construction?

There are many ways we could do this. For example, some provinces, such as Prince Edward Island, offer Down Payment Assistance Programs, which provide young homebuyers with low-interest loans to help them meet their down payment requirements. These programs could be expanded (or made federal), but applied to new housing only. Alternatively, a two-tier downpayment requirement system could be created, where the minimum down payments are lowered for purchasers of new homes. Ideally, this would be coupled with CRA income verification for mortgages.

If governments were to get creative, they could refine their existing policies that promote homeownership, which boosts demand for all forms of housing, and instead target them towards new housing only, as a way to help boost housing construction.

We cannot delay: It’s time to boost supply by boosting demand for new

The ideas presented in this piece scratch the surface of what is possible. Given the aggressive housing supply targets set by provincial and federal governments, coupled with the sharp decline in new housing sales in markets such as Vancouver and Toronto, time is of the essence. It’s time to boost the demand for new homes in Canada.

Download a PDF of this article here: